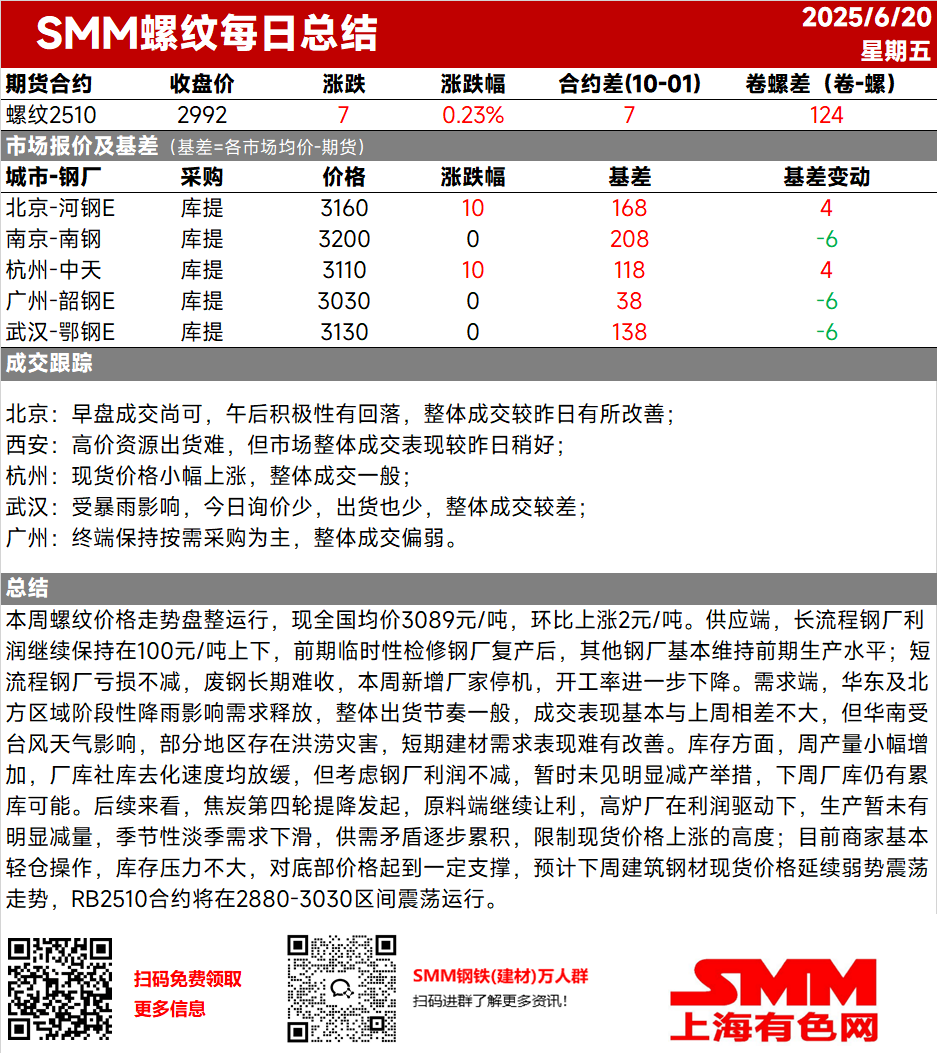

This week, rebar prices consolidated, with the nationwide average price at 3,089 yuan/mt, up 2 yuan/mt MoM. On the supply side, blast furnace steel mill profits remained around 100 yuan/mt. After the temporary maintenance steel mills resumed production earlier, other steel mills largely maintained their previous production levels. EAF steel mills continued to incur losses, and steel scrap collection remained difficult over the long term. This week, additional manufacturers halted operations, leading to a further decline in the operating rate. On the demand side, intermittent rainfall in east China and northern regions affected demand release, with overall shipment rates being average. Trading performance was largely similar to that of the previous week. However, in south China, affected by typhoon weather, some areas experienced flooding, making it difficult for short-term construction steel demand to improve. In terms of inventory, weekly production increased slightly, and the destocking rates of in-plant and social inventory both slowed down. However, considering that steel mill profits remained unchanged, no significant production cuts were observed for the time being, and there is a possibility of inventory buildup at steel mills next week. Looking ahead, the fourth round of coke price reduction proposals has been initiated, with raw material costs continuing to decline. Driven by profits, blast furnace steel mills have not significantly reduced production yet. With demand declining during the off-season, the supply-demand imbalance is gradually accumulating, limiting the upside potential of spot prices. Currently, merchants are generally operating with light inventories, and inventory pressure is relatively small, providing some support to the floor price. It is expected that next week, the spot price of construction steel will continue to fluctuate rangebound, and the RB2510 contract will exhibit sideways movement within the 2,880-3,030 range.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)